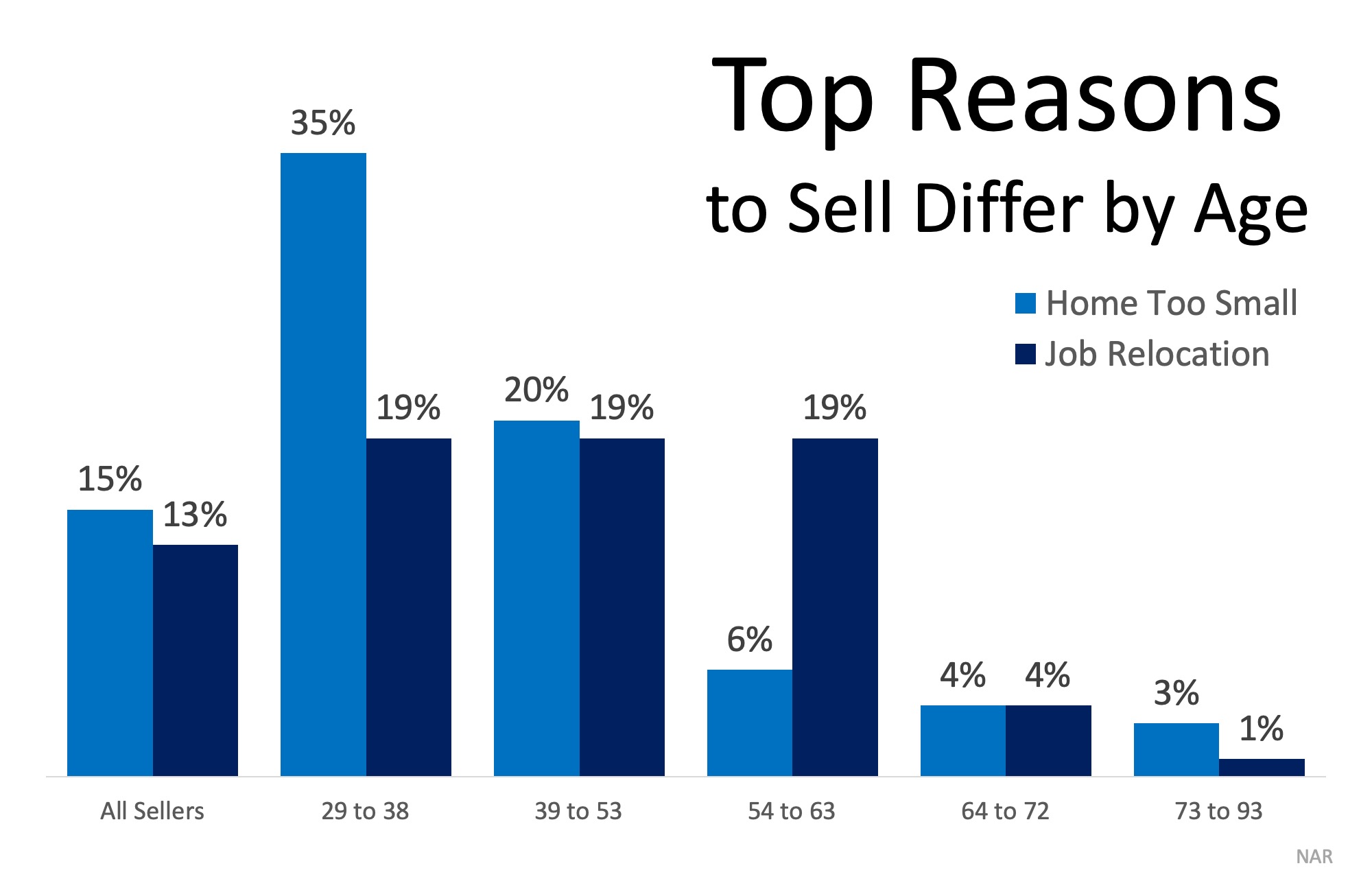

Over the last several years, many “baby boomers” have undergone a metamorphosis. Their children have finally moved out and they can now dream about their own future. For many, a change in lifestyle might necessitate a change in the type of home they live in.

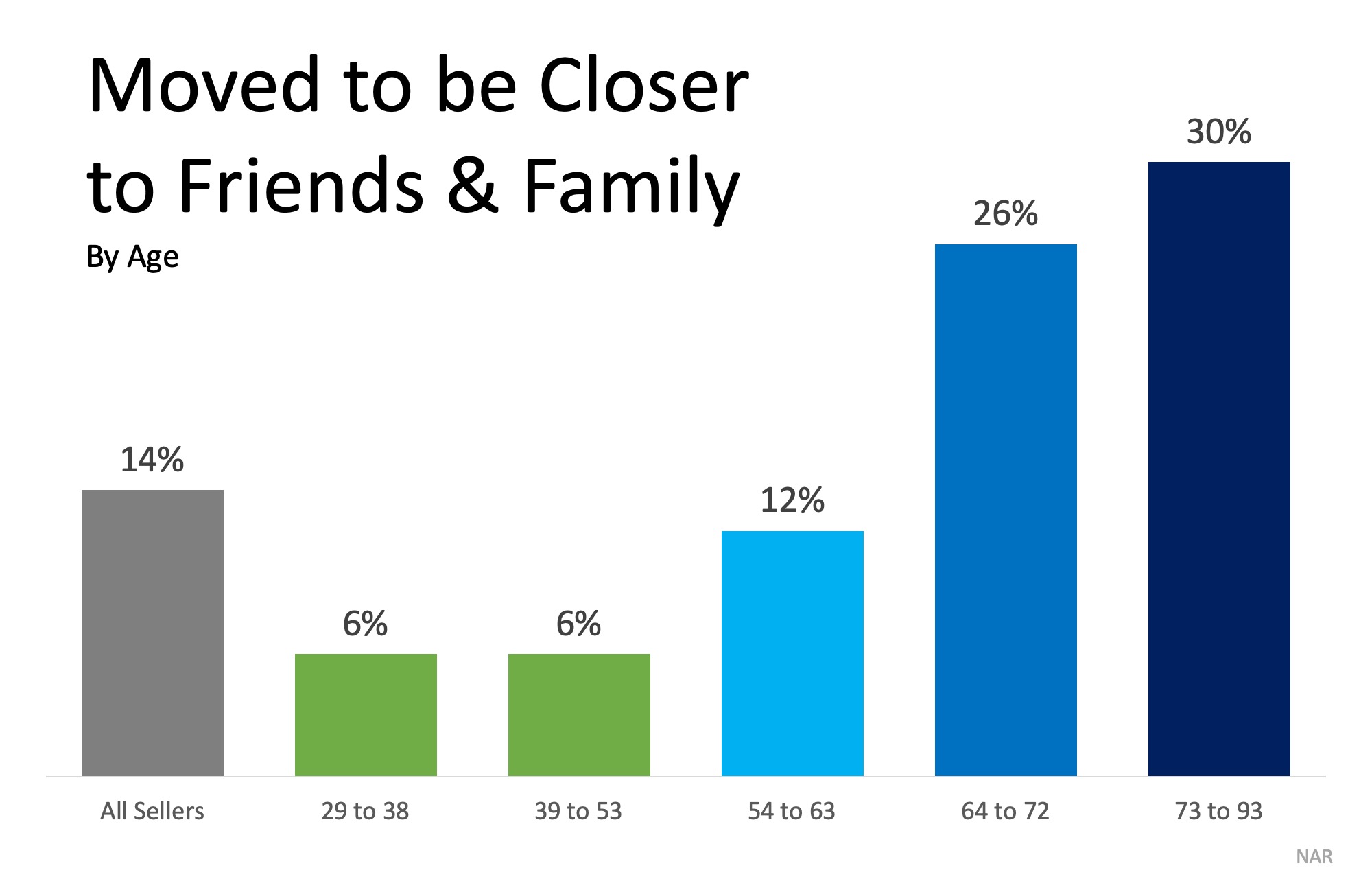

That two-story, four-bedroom colonial with three bathrooms no longer fits the bill. Taxes are too high. Utilities are too expensive. Cleaning and repair are too difficult. When they decide to travel to be with friends and family, locking up the house is too time-consuming and worrisome.

Instead, a nice ranch home with 2-3 bedrooms and two baths might better fulfill their new needs and lifestyle. The challenge many “boomers” have faced when trying to downsize to the perfect new home has been a lack of inventory.

The average number of years a family stays in their home has increased by fifty percent since 2008, causing fewer houses to come to the market. During the same time, new home builders were concentrating most of their efforts on large, luxury, expensive houses.

However, that is starting to change.

According to the U.S. Department of Housing and Urban Development and the U.S. Census Bureau, sales of newly built, single-family homes rose to a seasonally adjusted annual rate of 692,000 units in March. The great news is that more of those homes were sold at the lower end of the price range.

In a press release last week, the National Association of Home Builders (NAHB) explained that:

“The median sales price was $302,700, with strong gains in homes sold at lower price points. The median price of a new home sale a year earlier was $335,400.”

NAHB Chief Economist Robert Dietz offered further detail:

“We saw a large gain at lower price points where demand is strong. In March of 2019, 50% of new home sales were priced below $300,000, compared to 39% in March of 2018.”

Bottom Line

If you are a “boomer” thinking of selling your old house in order to buy a new home that better fits your current lifestyle, now may be the perfect time!

Source: Keep Current Matters Feed

Follow

Follow

![Existing Home Sales Slow to Start Spring [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/04/23164814/20190426-Share-KCM-549x300.jpg)

![Existing Home Sales Slow to Start Spring [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/04/23164805/20190426-EHS-Report-ENG-MEM.jpg)

![5 Reasons Why Millennials Buy a Home [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/04/09111636/20190419-Share-KCM-549x300.jpg)

![5 Reasons Why Millennials Buy a Home [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/04/09111414/Millennials-Choose-to-Buy-ENG-MEM1.jpg)