If you’re a homeowner thinking about making a move, you may wonder if it’s still a good time to sell your house. Here’s the good news. Even with higher mortgage rates, buyer traffic is actually picking up speed.

Data from the latest ShowingTime Showing Index, which is a measure of buyers actively touring homes, helps paint the picture of how much buyer demand has increased in recent months (see graph below):

As the graph shows, the first two months of 2023 saw a noticeable increase in buyer traffic. That’s likely because the limited number of homes for sale kept shoppers looking for homes even during colder months.

To help tell the story of why the latest report is significant, let’s compare foot traffic this February with each February for the last six years (see graph below). It shows this was one of the best Februarys for buyer activity we’ve seen in recent memory.

In the last six years, we saw the most February buyer traffic in 2021 and 2022 (shown in green above), but those years were highly unusual for the housing market. So, if we compare February 2023 with the more normal, pre-pandemic years, data shows this year still marks a clear rise in buyer activity.

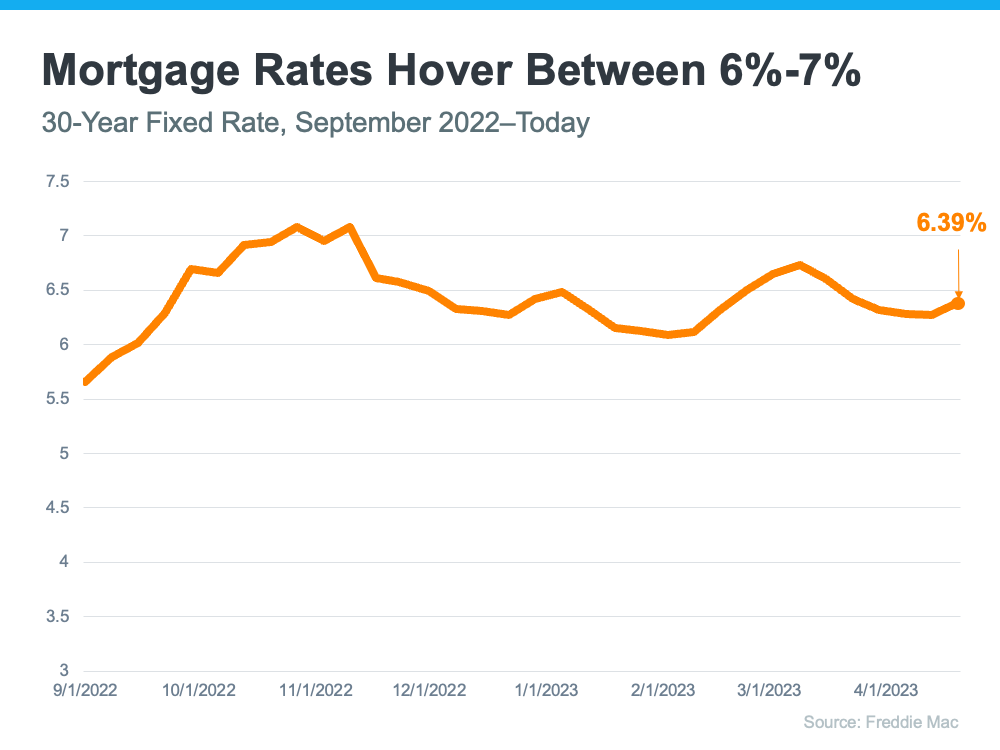

The uptick in buyer traffic is even more noteworthy considering the increase in mortgage rates this February. The Freddie Mac 30-year fixed mortgage rate rose from 6.09% during the week of February 2nd to 6.50% in the week of February 23rd. But even with higher rates, more buyers were looking for a home.

Jeff Tucker, Senior Economist at Zillow, says the increased buyer activity could continue:

“More buyers will keep coming out of the woodwork. We always see a seasonal uptick in home shoppers in March and April . . .”

If you’re looking to sell your house, seeing buyers still active in the market this year should be encouraging. It’s a sign buyers are out there and could be looking for a home just like yours. Working with a real estate professional to list your house now will help you get your home in front of eager buyers today.

SBottom Line

Rising foot traffic is a bright spot for this year’s housing market and indicates that buyers are looking to purchase this year, even with higher mortgage rates. If you’re ready to sell your house, partner with a real estate professional.

Source: Keeping Current Matters

Follow

Follow

![Ways To Overcome Affordability Challenges in Today’s Housing Market [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/content/images/20230428/Ways-To-Overcome-Affordability-Challenges-In-Todays-Market-KCM-Share.png)

![Why You May Want an Energy-Efficient Home [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/content/images/20230420/Why-You-May-Want-An-Energy-Efficient-Home-KCM-Share.png)